Living on the Texas coast changes the roofing equation. Salt air corrodes exposed metal fasteners. UV radiation degrades shingle granules faster than inland. Hurricane-force winds test every seam, nail, and connection. Materials rated for 20–30 years nationally may only last 15–20 years in Corpus Christi’s demanding environment.

That’s why choosing a local contractor who understands coastal roofing is critical. RISE Roofing is an Owens Corning Certified Installer. We’re also certified by Owens Corning, DECRA, and Tilcor. Every roof we install meets or exceeds TWIA windstorm requirements, and we handle WPI-8 certification in all designated zones.

Look for missing or curled shingles, dark streaks (algae growth from coastal humidity), granule accumulation in gutters, or any visible daylight through the attic. After any named storm, schedule a professional inspection even if the roof looks fine from the ground — hail and wind damage are often invisible without close-up examination. Call (361) 208-0885 for a free inspection.

For upfront affordability, 130mph-rated architectural shingles at $8,000–$14,000 offer strong storm protection. For long-term value, standing seam metal at $24,000–$32,000 lasts 40–60 years with near-zero maintenance and insurance premium savings of $500–$1,200/year. Over 20 years, metal is often cheaper despite the higher initial cost.

Yes. Every inspection is free with no obligation. We use drone imaging and hands-on assessment to evaluate your roof’s condition, then provide a written report and estimate within 24 hours. Call (361) 208-0885 or schedule online.

Whether you’re dealing with storm damage, an aging roof, or planning a proactive upgrade, the right information helps you make better decisions. Corpus Christi’s coastal environment demands roofing solutions designed specifically for wind, salt, heat, and humidity. Contact RISE Roofing at (361) 208-0885 for personalized guidance and a free inspection with drone imaging, moisture testing, and a detailed written report. We serve all of Corpus Christi, Portland, Rockport, Aransas Pass, Port Aransas, Padre Island, and surrounding Coastal Bend communities. 24/7 emergency response available.

TWIA (Texas Windstorm Insurance Association) coverage requirements for Coastal Bend properties add a layer of complexity to insurance decisions. WPI-8 certification is mandatory after roof work. Understanding your policy's coverage type, filing deadlines, and supplemental claim procedures can mean the difference between full coverage and significant out-of-pocket costs when roof damage occurs in Corpus Christi.

RISE Roofing handles complete claims documentation for Corpus Christi homeowners — from initial damage assessment through adjuster coordination and supplement filing for hidden damage discovered during tear-off. Our insurance coordination service is included at no additional cost on all Corpus Christi-area projects. Call (361) 208-0885 for a free assessment.

Unlike inland Texas where hail is the primary threat, Corpus Christi's roofing challenges center on wind resistance, salt spray corrosion, and moisture management. RISE Roofing specifies corrosion-resistant fasteners, wind-rated attachment systems, and moisture-impermeable barriers on every project — ensuring your roof performs through decades of Coastal Bend weather.

RISE Roofing provides free, comprehensive roof assessments across the Corpus Christi metro. Every assessment includes professional photo documentation, material recommendations tailored to your property's coastal exposure profile, and a fixed-price proposal. Serving North Padre Island, Flour Bluff, Portland, Rockport, Port Aransas, Ingleside, and Annaville.

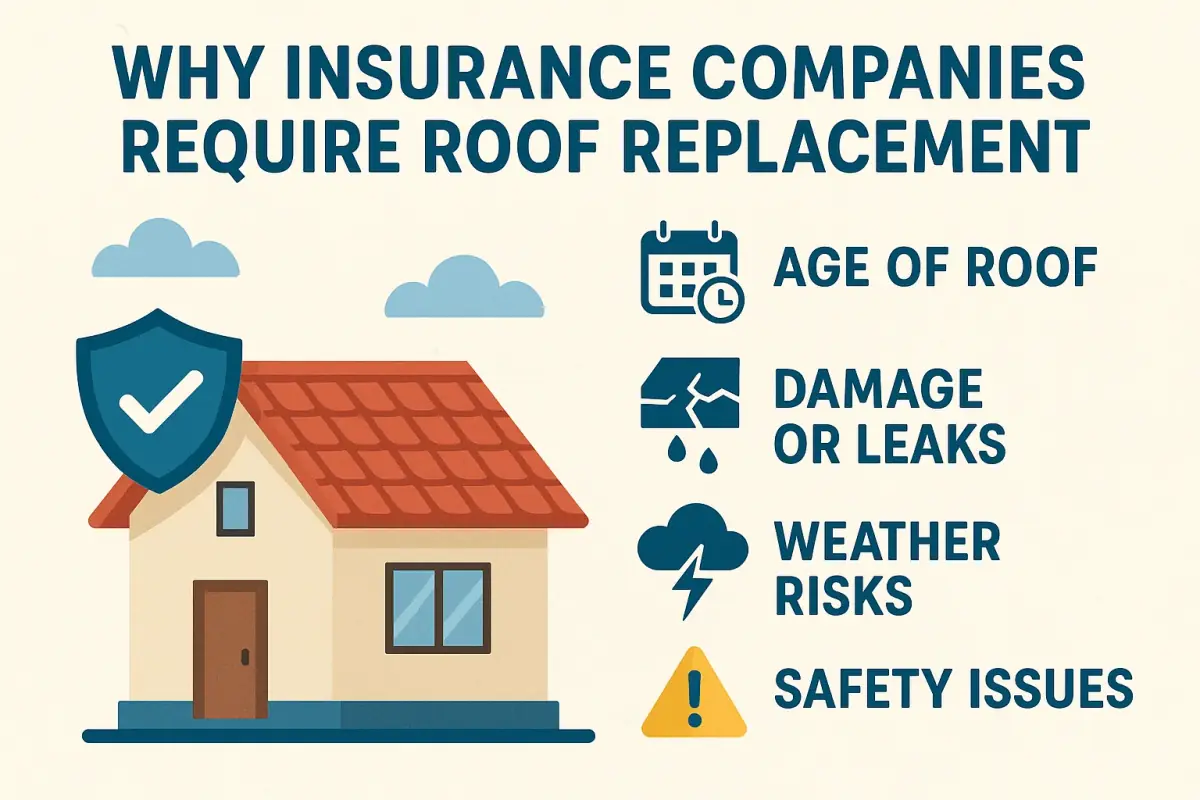

Making the roof replacement decision requires weighing several Corpus Christi-specific factors beyond simple age or visible damage. RISE Roofing evaluates four criteria during every assessment:

1. Structural integrity assessment. We perform core cuts and infrared moisture scanning to evaluate the deck and insulation beneath the visible membrane. Moisture trapped in insulation — common after years of exposure to salt air corrosion, hurricane winds, and coastal UV — cannot be solved by re-roofing over the existing surface. If more than 25% of insulation shows moisture, full tear-off and replacement of compromised sections is required.

2. Remaining service life calculation. Based on material type, current condition, and Corpus Christi's climate exposure profile, we project how many years of reliable waterproofing your current roof can still deliver. If remaining life is under 5 years and a storm event is statistically likely within that window, proactive replacement typically costs less than emergency repair plus accelerated replacement later.

3. Insurance position analysis. Your current roof's age and condition directly affect insurance coverage terms. TWIA windstorm coverage with mandatory WPI-8 certification — understanding how your carrier views your roof's condition before filing a claim helps you make strategic decisions about timing and material selection.

4. Total cost of ownership. We compare repair-to-maintain costs over the next 10 years against single replacement cost today. In Corpus Christi, where salt spray corrosion and Category 4 hurricane exposure creates ongoing maintenance demand, the break-even point typically favors replacement when repair costs exceed 30-40% of replacement value.

Current Corpus Christi residential replacement pricing: $4.50-$7.50/sqft for shingles, $12-$16/sqft for metal, $8-$14/sqft for commercial TPO. RISE Roofing provides detailed, line-item proposals with price guarantees locked for 30 days.

Understanding your roof insurance coverage before you need to file a claim puts you in a significantly stronger position. Corpus Christi homeowners should review their policy annually — specifically confirming whether they have Actual Cash Value (ACV) or Replacement Cost Value (RCV) coverage, understanding their deductible amount and type (flat dollar vs. percentage), and knowing the claim filing deadline after a covered event.

The difference between ACV and RCV coverage is substantial in practice. With ACV, your insurer deducts depreciation based on your roof's age and condition before issuing payment — meaning an older roof in Corpus Christi may receive only 40-60% of the replacement cost. RCV policies pay the full replacement cost minus your deductible, with any depreciation holdback released after you complete the repair. For Corpus Christi properties in areas with frequent weather events, RCV coverage provides meaningfully better financial protection.

Filing and managing a roof insurance claim while simultaneously dealing with property damage is overwhelming. RISE Roofing provides complete claims coordination for Corpus Christi homeowners at no additional cost — this includes initial damage documentation, adjuster meeting attendance, scope-of-loss review, supplemental claim filing for hidden damage discovered during tear-off, and final payment reconciliation.

Texas law protects your right to choose your own roofing contractor regardless of what your insurance company recommends. You are not required to use your insurer's "preferred vendor" list, and your contractor choice cannot affect your claim eligibility or payout amount. RISE Roofing works with every major insurance carrier serving Corpus Christi and understands the documentation standards each requires. Call (361) 208-0885 for a free damage assessment.

RISE Roofing provides complimentary roof assessments for homes and commercial properties across the Corpus Christi metro — from North Padre Island and Flour Bluff to Portland, Rockport, and Port Aransas. Every assessment includes professional photo documentation, material recommendations tailored to Coastal Bend conditions, and a fixed-price proposal locked for 30 days. As certified installers for Owens Corning, DECRA, and Tilcor, we deliver manufacturer-backed warranty coverage that protects your investment through decades of coastal weather. Contact us at (361) 208-0885 or fill out the form to schedule your free evaluation.

RISE Roofing has earned the trust of Coastal Bend property owners through a combination of manufacturer certifications, TDI-compliant installations, and a track record of standing behind our work through every hurricane season. Our certifications from Owens Corning, DECRA, and Tilcor mean every installation carries manufacturer-backed warranty coverage — not just contractor promises. We specify corrosion-resistant fasteners, wind-rated attachment systems, and moisture barriers calibrated for the salt air, hurricane winds, and intense UV that define Corpus Christi's coastal environment.

Every RISE Roofing project begins with a free, comprehensive assessment — including satellite and drone measurements, material recommendations, and a fixed-price proposal with no hidden costs. We handle permit applications, insurance coordination, and manufacturer warranty registration as standard parts of our service. For Corpus Christi homeowners and property managers across North Padre Island, Flour Bluff, Portland, Rockport, Port Aransas, and the entire Coastal Bend, RISE Roofing delivers the quality and reliability that coastal properties demand. Call (361) 208-0885 to schedule your free evaluation.

RISE Roofing provides residential and commercial roofing services across Corpus Christi, Portland, Rockport, Aransas Pass, Port Aransas, North Padre Island, Ingleside, Flour Bluff, Annaville, and surrounding communities. As an Owens Corning Certified Installer serving the Coastal Bend, we deliver top-tier certified roofing.

Every roofing project we take on includes: a free pre-installation inspection with drone imaging, windstorm-rated materials that meet or exceed TWIA requirements, WPI-8 certification in all designated zones, proper hurricane clip installation, enhanced underlayment for wind-driven rain protection, and a final quality inspection before we consider the job complete. We also offer $0 down financing with rates from 6.99% APR through 20+ lending partners.

Whether you’re dealing with storm damage, planning a proactive replacement, or need a second opinion on another contractor’s quote, call (361) 208-0885 for a free, no-pressure consultation. We’re available 24/7 for emergencies.

Insurance guidance from the Texas Department of Insurance.

🔒 Free, no-obligation quote — Price-locked estimate in 24 hrs

Trace your roof on satellite imagery and get a real installed price in under 60 seconds.

Powered by satellite roof measurement technology. No obligation.